CIO Viewpoint: China Two Sessions

China held its “two sessions” meeting last week. They are named the two sessions for the simultaneous meetings of the second in a series of the NPC (National People’s Congress) and CPPCC (Chinese People's Political Consultative Conference). We focus below on four takeaways from the meetings and link them to the three global mega-trends underpinning our Investment Committee’s thematic investment strategy.

China encompasses all our key global trends on which we align our thematic investment ideas: (1) a drive to increase consumption of its rising middle class consumer (2) improving social services including healthcare, for China’s ageing population, and (3) desire to become a disruptive leader and innovator in information and energy technology.

Trend 1: The Rise of the Middle Class Consumer

2019 Gross Domestic Product (GDP) year over year growth estimate of 6 to 6.5% was widely reported as the headline take-away. However, more critically, we think China still needs to transition its GDP equation to command a greater percentage of domestic consumption of services, most especially; it’s an inevitable part of the migration from emerging market to an advanced economy. A typical advanced economy’s personal consumption level is approximately 70% of GDP (BEA, Bureau of Economic Analysis). China has not seen that level since the 1960s. Currently China’s personal consumption as a percentage of GDP is ~40% (CEIC, Census and Economic Information Center). We think there is more room for it to expand.

China is likely to indirectly encourage increases in domestic consumption through fiscal stimulus measures and their resulting effect on GDP.

Cut corporate tax burden by nearly 2 trillion yuan (~ US$ 300 bn) in 2019

- China will reduce the tax burdens and social insurance contributions of enterprises by nearly 2 trillion yuan (about 298 billion US dollars) this year.

- The reduction of tax burdens will primarily focus on the manufacturing sector and on small and micro businesses.

- China will reduce the current value-added tax rate of 16 percent for manufacturing and other industries to 13 percent, and lower the rate for such industries as transportation and construction from 10 percent to 9 percent.

There is ongoing investor concern that China is over leveraged and over extended on its corporate debt. We see action to be taken from two angles: (i) increasing lending through non-traditional lenders by way of FinTech (Financial Technology) and thus leveraging on China’s technology-lapping, and (ii) calls to limit provincial SOE borrowing so as to shift from debt-led growth to one fueled by privately owned small businesses, who ordinarily provide more high quality and sustainable growth contributions to GDP than government run enterprises would provide in the long-run. We think these are prudent reforms that make China more akin to an advanced economy.

Alleviate the financing restrictions on private small and micro enterprises

- Chinese government aims to 1) expand credit supply and reduce borrowing rate to private small and micro enterprises, 2) increase medium and long-term loans to manufacturing companies.

Trend 2: Ageing Population

Develop the pension service industry

- Chinese population of over 60 years old has reached 250 million. Chinese government will continue to focus on developing the pension service industry, especially the community-based pension service.

- In addition, the Chinese government will offer tax reductions, financial support as well as water and electricity thermal price concessions for retirement homes.

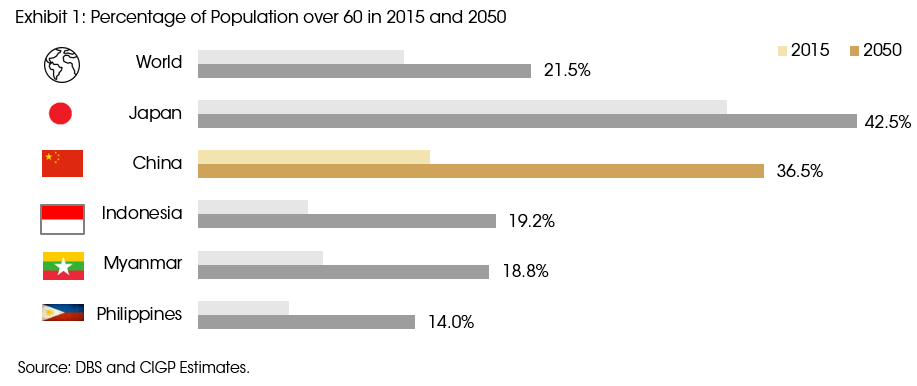

China’s over 60 demographic is expected to be approximately 36.5% of its population by 2050 (DBS). [See Exhibit 1.] And while their consumption (”C”) habits are far different than families and millennials, this population too requires services that will help to stimulate that “C” part of Y = C + I + G + (X - M) equation.

As highlighted in the February 2019 CIO Newsletter, we like insurance and select healthcare segments such as drug distribution and medical devices and equipment.

Trend 3: Disruptive Technologies

Support the growth of emerging industries

- Chinese government will continue to support the industry development in research & development of big data, artificial intelligence, information technology, biomedicine, new energy vehicles and new materials.

- The subsidies to new energy vehicles will remain to stimulate consumption of EV.

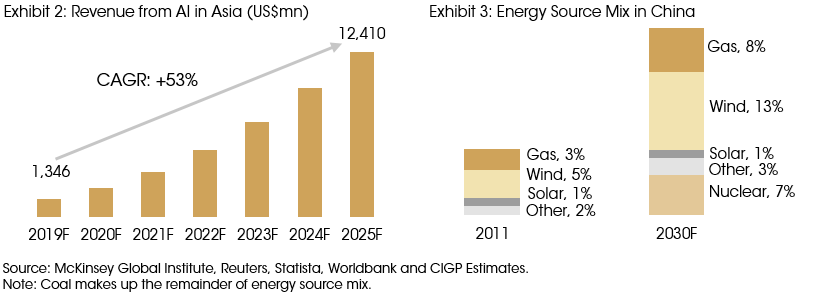

China is on a resolute path to become a global technology leader – in both information and energy. China’s “new economy” is building and subsidizing leading AI technologies to help domestic China improve daily living standards and reduce its labor costs. Exhibit 2 shows the forecasted revenues from government, consumer and enterprise markets garnered from AI technology in Asia. China is fostering the Greater Bay Area, which includes Hong Kong, Macau, Shenzhen, Guangzhou and the Guangdong province, a de-facto technology zone parallel with California's Silicon Valley.

Furthermore, revitalizing China’s energy grid to meet carbon emission targets are front and center of its economic goals. [See Exhibit 3.] Lateral to this, China still aims to have 40% of vehicles on the road run by battery technology by 2025. This is a lofty goal and outruns any other developed market country’s regulation. But is also helps meet emission goals.

We tend to avoid the volatility of technology stocks in China, but find attractiveness in the sector’s bonds. While a ‘trade war’ is now thankfully becoming a ‘trade resolution’, we think such outcome will ultimately disappoint markets on a headline basis. However we have identified two auto supply chain companies that are likely to benefit from China’s electric vehicle goals. Our multi-asset Asia-Pacific model and portfolio has exposure to a steering systems manufacturer, and a moldings manufacturer.

Growing but not forgotten

China is still growing, not contracting, its economy; this is important to note. All of our global mega tends are representative in China’s new economy, thus our preference to China in Asia and in emerging market weightings in asset allocation portfolios. We would look for updates from China on Belt and Road, Made in China 2025, if any, monitor international relations and most especially for investors, we expect further financial market reform and integration with the Greater Bay Area.

We believe China will transform its GDP equation to command a greater percentage of domestic consumption. Coupled with fiscal stimulus, social service expansion and promoting technology leadership, China’s economy will likely avoid a hard landing and achieve the economic stability that it desires.