CIO Viewpoint: Switzerland's Economy

Consumers in Switzerland

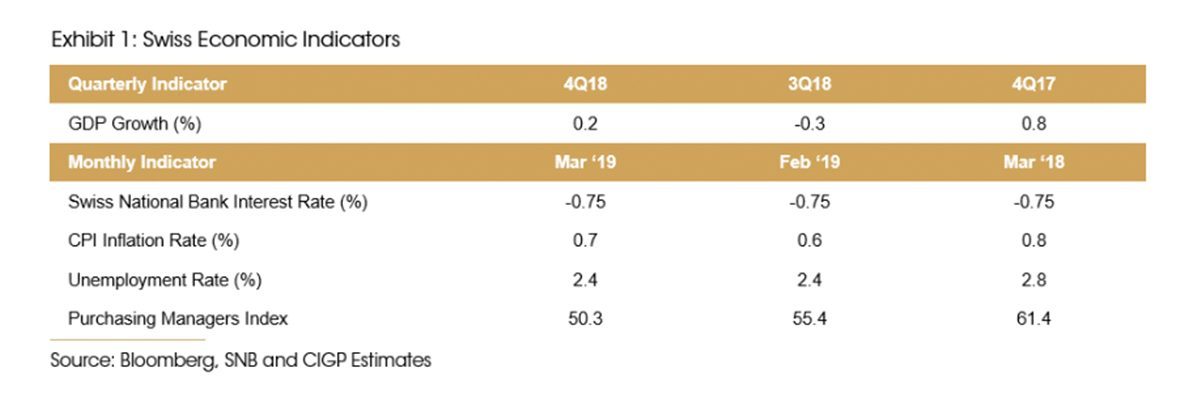

Switzerland is likely to suffer from a weakening global economy; it is already under pressure from a weak Europe including Italy’s 2018 recession and Germany’s sub-50 PMI since January. Germany is Switzerland’s number one export partner (~18% of total exports). Normally we would look to a domestic Switzerland to make up the difference in the interim, but we are not convinced a domestic Swiss consumer can exclusively fend off declining growth or even a bout of recession despite low unemployment (average 2.4% p.a.), reasonable wage growth and very low inflation (0.7% p.a.) — the latter being a key facet of household consumption.

We find solace that Switzerland and the UK signed a trade deal in February. However, the UK is hardly a top 5 export market, at some 3% of total exports (OEC, Observatory of Economic Complexity, MIT) . Economic troubles in some of the largest economies in the world and Switzerland’s largest export markets: Germany, US and China will likely impact Swiss export growth. A strengthening Franc will not help the situation. Furthermore, too much of Swiss financial assets are tied up in real estate of which the SNB is closely following for any signs of erratic development that could disrupt its economic growth.

We suggest investing in innovative Swiss multinationals tied to global mega trends not reliant on the Swiss economy while taking minimal exposure to the Franc (CHF) in portfolios and watch for any signs of trend line disruption on the Franc/Dollar/Euro trajectory. For example, pharmaceutical exports are less sensitive to FX movements and economic cycles in contrast to Swiss industrials which will likely be weakened by trade tensions and lower manufacturing activity.

The SNB and GDP

In Q3 2018 Swiss GDP turned negative, which is normally a culmination of weak economic data that points to a worrying sign of a recession of which history (2002 and 2012) gives us some transparent examples. This year, UBS is more bearish then the SNB, and estimates 1% GDP growth for 2019 which is even lower than their original 2019 estimate and the actual GDP growth in 2018. The SNB still forecasts 1.5% 2019 GDP growth.

The SNB does not particularly differentiate itself from its peer central banks. It is more or less bound to move in lock step with the ECB. The SNB is likely to raise rates if and when the ECB begins, which we estimate to be in early 2020 at this juncture. Negative interest rates since 2015 in Switzerland and its high financial literacy and investor’s insatiable demand for yield has pushed Swiss investors to real estate and non Franc assets. A weaker CHF has not enhanced those returns when translated to local currency. Recent comments from SNB’s members of the Governing Board gave indications that they can afford to stay cautious and still have room to further cut rates if needed. The most likely reason for the SNB to increase rates before the ECB would be to control a sustained surge of inflation.

Therefore, we do not expect the SNB to change its outlook much, other than the usual forecast adjustments which are unlikely to affect its interest rate trajectory. We do not think the SNB will raise rates until 2020. Switzerland is reliant on export growth followed by household consumption and not natural resources prices, on which Norway is reliant, which allows it to raise rates.

The Sound Swissy

The CHF has been relatively weak for several years owing in large part to the generally stronger dollar trend. We think this has likely kept Swiss exports afloat by making them price attractive. Exports slowed (+0.1%) in March but still grew at a much slower pace than February (+1.5%). This is likely due to slowing demand than a strengthening currency. If we saw a rapid strengthening in the CHF vs EUR or USD we would be concerned. This is all too probable given the relationship between the EUR and USD which moved quickly in 2017 and 2018.

Additionally, negative yielding assets in CHF have forced investors to take riskier bets on higher return assets and more liquid assets such as stocks and funds but also seemingly basic bond funds as a quasi cash equivalent.

While the Franc is still marked by some as a safe haven currency, competing with gold in times of financial stress, there were short periods in 2018 when the Yen was a lateral safe haven currency for global investors. Negative interest does not make the CHF an in demand funding currency. Japan’s equally fiscally stable export oriented economy, the fourth largest in the world, has become an investors' friend for funding the carry trade at certain cycles of the calendar year. The effect of the carry trade has become more important as most global central banks are dovish and in rate pause periods.

United Kingdom and Switzerland Trade Agreement

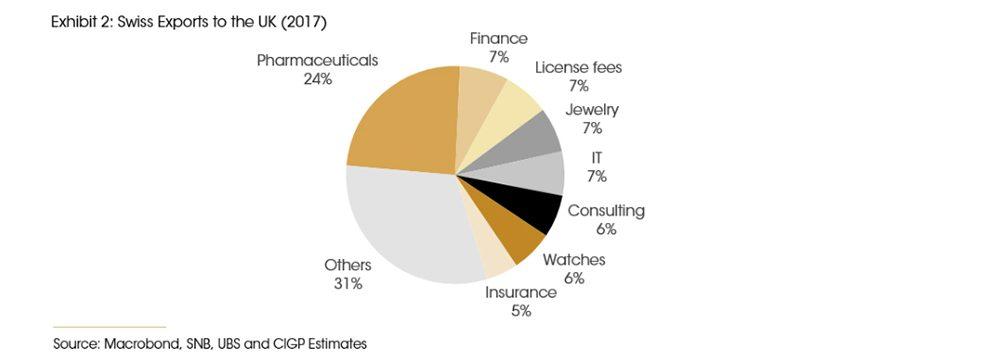

In February, Switzerland and the UK signed a joint trade continuity agreement in advance of the UK's exit from the European Union. The agreement with the UK will ensure continued tariff waivers and expeditious customs clearance in accordance with existing preferential parameters. Items such as clocks, watches and prescription medicines will enable UK consumers to maintain choice and Swiss exporters to ensure they continue to have a demand market for their exports despite that market’s dis-connection from the broader Economic Union.

While the UK is not in the top 5 export market for Switzerland, a loss of trade flow between the UK and Switzerland could have been a blow to Swiss exports especially for vital packaged and prescription medicines. Maintaining ease of trade and continuing the standard elimination of duties, and tariffs will help to keep Swiss exports competitive in the fifth largest economy (UK) in the world.

We think these bi-lateral agreements will be beneficial to Switzerland and will increasingly be de-rigueur as global trade partners bifurcate from the multi-lateral approach.

Steady but Fragile

Switzerland is not immune to global trade disruptions or weakening global economies. After all China is its third largest trading partner (~9.2% of exports). With a strong financial services sector supporting employment, largely stable (and regulated) real estate prices, and low inflation may tide the Swiss economy over in the face of pending export weakness, the direction of the CHF remains the unknown. Franc investors are having to take on additional risk to garner return putting principal capital at risk more than is the case with non-Franc investors. We suggest investing in innovative Swiss multinationals tied to global mega trends that are not reliant on the Swiss economy while taking minimal exposure to the Franc in portfolios, and watch for any signs of trend line disruption on the CHF/USD/EUR trajectory.