Focus: Impact of Hong Kong Protests on Retail and Property

David Ho

The social unrest in Hong Kong (HK) has lasted throughout summer for over 15 weeks. It did not stop or calm down even after the Chief Executive, Carrie Lam, made a concession to “formally withdraw” the Fugitive Offender Bill which addressed one of the five demands from the protestors. HK’s economy and stock market have taken a heavy toll from these protests. As an asset manager on the ground, we believe the burning questions that investors may want to know is if there are investment opportunities as a result of the crisis, and what are the potential risks and rewards of such opportunities.

We think the best way to gauge the future is through the lens of history. We aim to provide our analysis on the impact of the protests on two of the most vital sectors in HK – the retail market and the property market.

Mainland Tourists as the Driving Force for Retail Growth

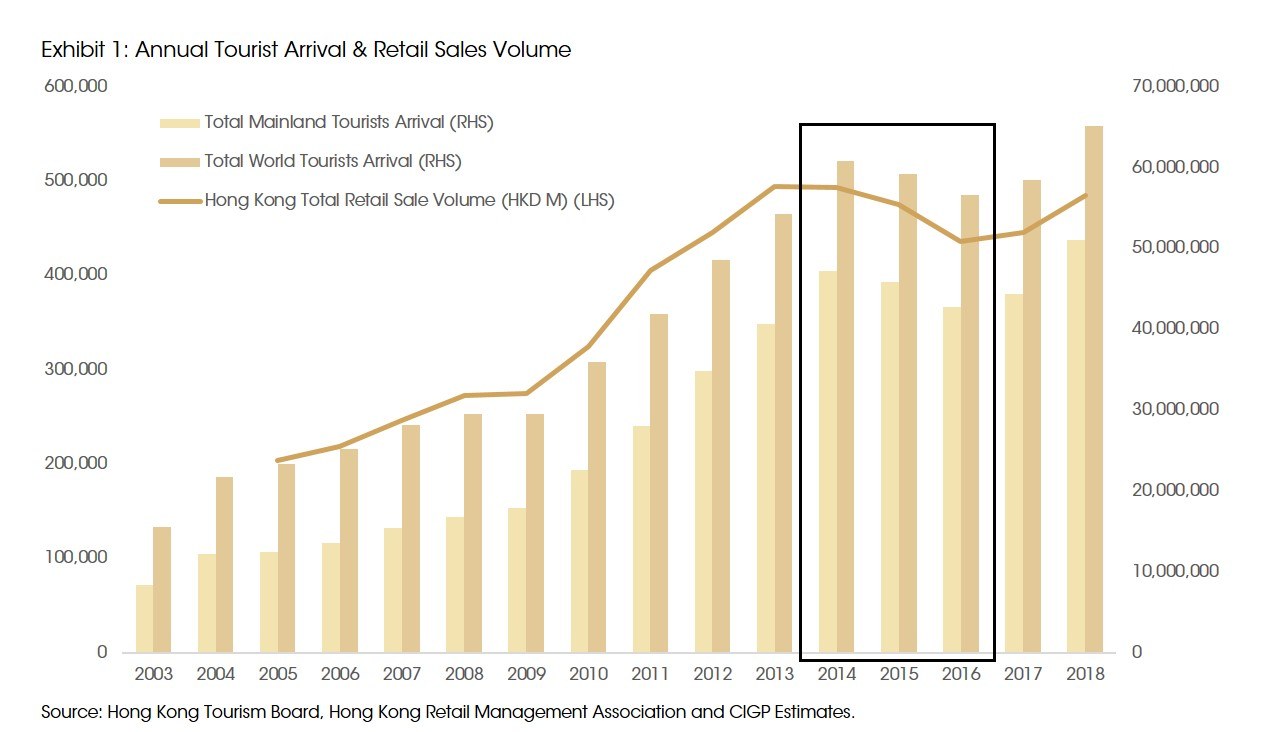

Since China approved the Individual Visit Scheme (IVS) to HK during the outbreak of SARS in 2003, the increasing arrival of mainland tourists has been a major driver of retail sales growth. The share of mainland tourists among the total visitors coming to HK has increased from ~55% in 2003 to ~80% as of 2019. Between 2014-16, there was a decline in mainland tourists. Unsurprisingly, the retail sector also experienced a contraction for 3 consecutive years.

The Difference Between Now and 2014

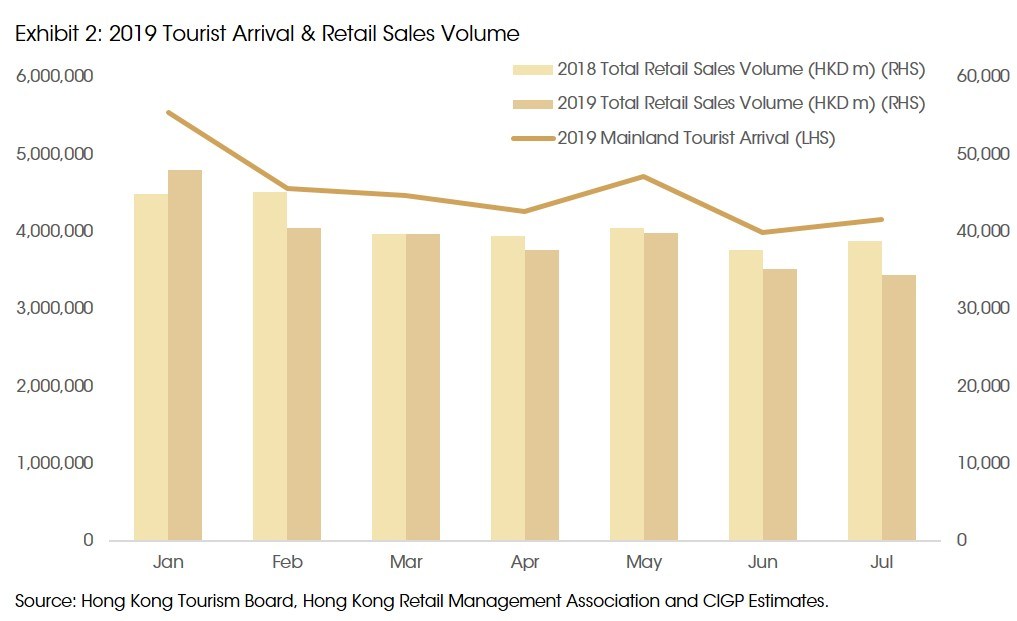

As the current protest continues to escalate and when comparing the current situation to the 2014 Occupy Central movement, we see a similar impact in the short run and major differences in the long run. According to the latest statistics from HK Retail Management Association, an independent retail representative organization that started in 1983, the value of total retail sales in July 2019 declined by 11.4% compared to July 2018. Retail sales have been declining for the past six consecutive months, starting in February 2019. This had not been seen since 2014-2016. Under these difficult times, commercial property owners will likely be unable to increase the rent of retail spaces, and may even have to lower the rent in order to keep their tenants.

While we cannot attribute the 2014-16 decline in retail to the 2014 protests completely, we believe that the impact of these two protests on tourism will be different. The current level of violence and anti-Chinese sentiment appears to be at an all-time high, and we believe that this could possibly cause the Chinese government to reconsider its policy towards HK. Consumption could be re-directed back into China, and the gradual expansion in IVS visa could turn into tightening instead. We do not see a recovery in the short term and think a return to growth remains highly uncertain. We see structural scars that have been made regardless of how the protests evolve from this point on.

The Risk and Opportunities in Retail and Commercial Property Investments

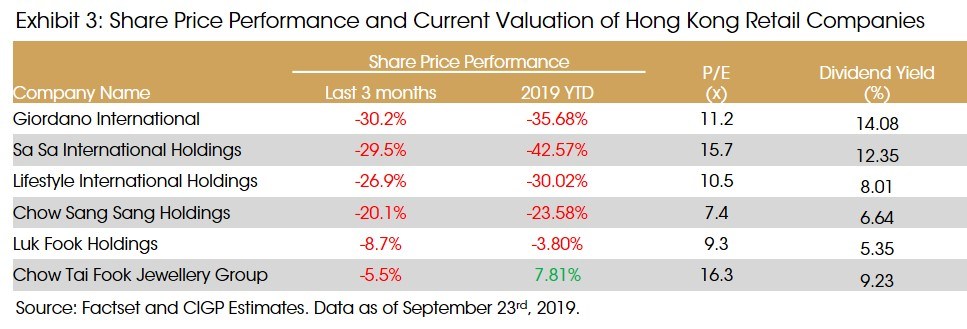

Retail and property stocks have corrected significantly over the past 6 months, particularly those that have concentrated exposure to the HK market. Despite the fact that some retail stocks are currently trading at a low valuations and have high single digit dividend yields, we do not recommend buying into the sector. The lack of new growth catalysts could mean that current low valuations are just value traps. Nonetheless, there are rare opportunities that could be identified occasionally when shares over-correct. Even though the retail sector rallied excessively in excitement of the HK government formally withdrawing the bill, the sector quickly returned all its gains. We recommend investors to avoid catching the falling knife in the HK retail sector. Commercial property owners that have a large exposure to shopping malls should also be avoided due to difficulties they will face.

Residential Property Developers

With all the affordability metrics indicating that HK property is the most unaffordable around the world, one would expect that the current social unrest could be the perfect catalyst for property price to fall from its shaky ground. For us, however, the real question has always been supply and demand.

Limited Property and Land Supply

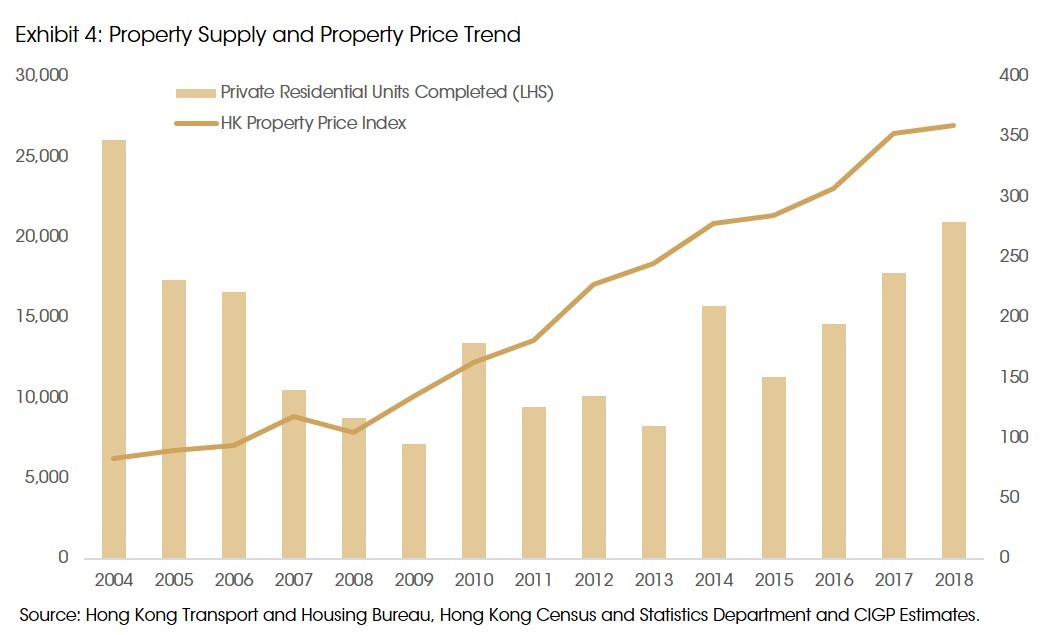

Despite the common perception that land is scarce in HK, the truth is that only 7% of total land available is developed into residential property. 75% of total land has remained untouched and is considered “Non-spade ready”. This type of land, according to estimates from the HK Task Force on Land Supply, would take 11 to 14 years to convert into usable land for residential property.

According to the statistics from the Transport and Housing Bureau, the government expects 93,000 private residential units to be available in the coming 3-4 years. This translates to roughly the same number of private residential units available last year. However, taking into account the fact that past estimates have a track record of missing their target, and the latest private residential unit commenced construction in 2019 Q1 is 58% lower than 2018 Q1, the estimate will likely be revised downward. Given that the government is currently in a weak spot in terms of public support, we expect that any effort to increase land supply by converting “non-spade ready” land will be blocked in the Legislative Council. Without massively increasing land supply, it would be impossible for property supply to increase dramatically.

Property Demand – Not All Demand is Equal

Demand for housing in HK is difficult to measure. For us, “demand” is defined as those who are willing, and more importantly, able to afford, instead of simply having the desire to purchase. A close proxy for property demand would be to look at the population growth and income distribution.

HK population has been growing at around 0.8% per annum over the past years. The increasing population creates a natural demand for local properties. On the other hand, HK’s Gini Coefficient (a measure of income inequality) is one of the highest in the world. Although the income growth rate for households seems similar, the absolute scale is very different. The top 3 deciles earn as much as 10 times the monthly income of the bottom 3.

After years of economic prosperity in HK, with low unemployment rate, controllable mortgage leverage, asset price inflation, and high saving rates, the wealthier portion of the population can still afford to purchase properties. Local media has been continuously reporting over-subscription to new property sales.

Impact of the Protest to Residential Property

We do not see the current social movement affecting any of the fundamental demand and supply characteristics listed above. Therefore we believe that the negative impact would remain only on a sentiment level. Negative sentiment could possibly drive some fickle sellers with fragile financials to sell in fear, but there will be buyers out there ready to absorb the unit. More importantly, the majority of property owners, have low leverage and so no financial pressure to fire sell under the current low rate environment. With no forced sellers, limited supply and consistently strong demand, we only see a mild correction in our bearish scenario. We do not expect a free fall in residential property price unless the current protest causes unemployment rates to go up massively such as what happened during the 1998 Asian Financial Crisis.

The Risk and Opportunities in Property Developers

Property developers in HK have a strong balance sheet and a decent level of land reserves for future development. With our expectation that residential property prices will stay stable due to tight supply and strong demand, investors with the right risk appetite could consider looking into the sector for quality names that over-corrected during the current social unrest.

End Forecast

While there is no clear visibility on when the protest will end, we do expect that the crisis will eventually scale down as:

- More and more citizens grow impatient with the social distortion.

- Protestors themselves grow tired and fail to continuously participate in the movement

Our expectations are based on our observations of past events such as the 2014 Occupy Central movement, and other protests worldwide. No protest lasts forever, but the impact of this one could linger longer than expected, and not all investments are affected in the same way. We therefore believe that investors should remain selective should they wish to hunt for a bargain during the current crisis.

If you are interested to know more about our views, subscribe to our newsletter or reach out to our Research Team.

Sources: Bloomberg, Hong Kong Census and Statistics Department, Hong Kong Retail Management Association, Hong Kong Task Force on Land Supply, Hong Kong Tourism Board, Hong Kong Transport and Housing Bureau, South China Morning Post